Social Security and Medicare 2025 Trustees Reports

July 31, 2025

Social Security and Medicare 2025 Trustees Reports: It’s Time to Address Funding Concerns

Each year, the Trustees of the Social Security and Medicare trust funds provide detailed reports to Congress that track the programs’ current financial condition and projected financial outlook. These reports have warned for years that the trust funds would be depleted in the not-too-distant future, and the most recent reports, released on June 18, 2025, show that Social Security and Medicare continue to face significant financial challenges.

The Trustees of both programs continue to urge Congress to address these financial shortfalls soon, so that solutions will be less drastic and may be implemented gradually. Americans agree — in a survey conducted last year, 87% of those polled said that Congress should act now to address Social Security’s funding shortfall, rather than waiting years to find a solution.1

Despite the challenges, it’s important to keep in mind that neither of these programs is in danger of collapsing completely. The question is what changes will be required to rescue them.

More retirees and fewer workers

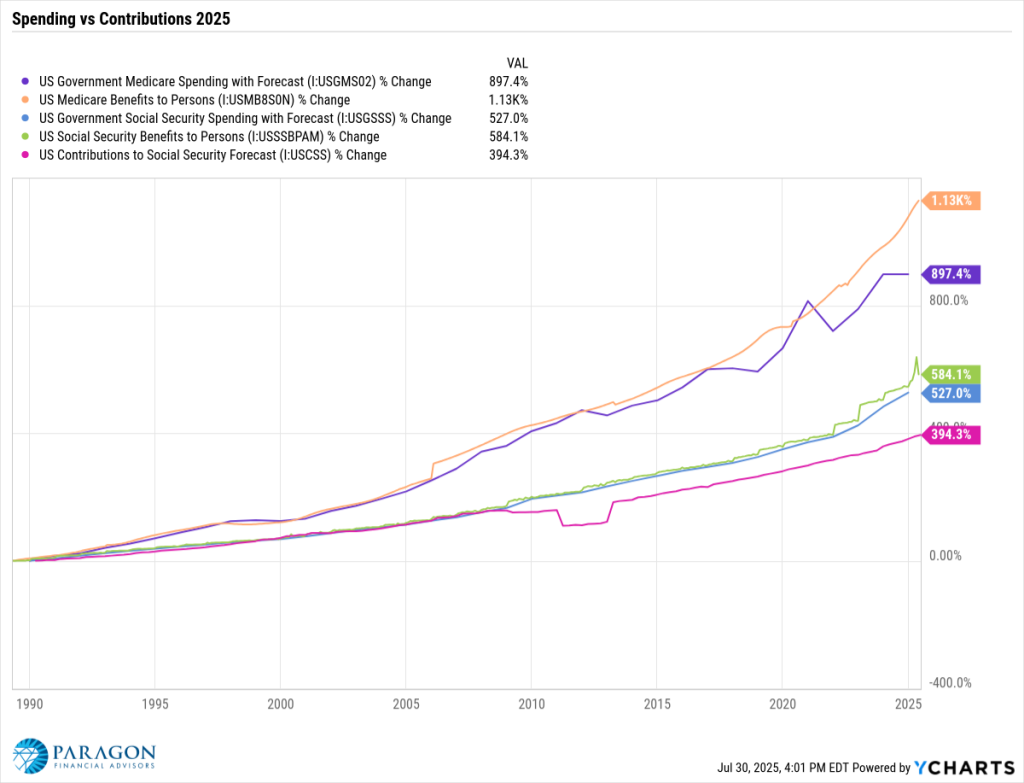

The fundamental problem facing both programs is the aging of the American population. Today’s workers pay taxes to fund benefits received by today’s retirees, and with lower birth rates and longer life spans, there are fewer workers paying into the programs and more retirees receiving benefits for a longer period of time. In 1960, there were 5.1 workers for each Social Security beneficiary; in 2025, there are 2.7, a number that is projected to drop to 2.2 by 2045.

Dwindling trust funds

Payroll taxes from today’s workers, along with income taxes on Social Security benefits, go into interest-bearing trust funds. During times when payroll taxes and other income exceeded benefit payments, these funds built up reserve assets. But now the reserves are being depleted as they are used to supplement payroll taxes and other income to meet scheduled benefit payments.

Social Security outlook

Social Security consists of two programs, each with its own trust fund. Retired workers and their families and survivors receive monthly benefits under the Old-Age and Survivors Insurance (OASI) program; disabled workers and their families receive monthly benefits under the Disability Insurance (DI) program.

The OASI Trust Fund reserves are projected to be depleted in 2033, unchanged from last year’s report, at which time incoming revenue would pay only 77% of scheduled benefits. Reserves in the much smaller DI Trust Fund, which is on stronger footing, are not projected to be depleted during the 75-year period ending in 2099.

Under current law, these two trust funds cannot be combined, but the Trustees also provide an estimate for the hypothetical combined program, referred to as OASDI. This would extend full benefits to 2034, a year earlier than last year’s report, at which time, incoming revenue would pay only 81% of scheduled benefits.

This year’s report states that the January 2025 enactment of the Social Security Fairness Act of 2023 is projected to have a substantial effect on Social Security’s financial status. This law repealed the Windfall Elimination Provision and Government Pension Offset, and consequently, increased Social Security benefits for some people who worked in jobs not covered by Social Security.

Medicare outlook

Medicare also has two trust funds. The Hospital Insurance (HI) Trust Fund pays for inpatient and hospital care under Medicare Part A. The Supplementary Medical Insurance (SMI) Trust Fund comprises two accounts: one for Medicare Part B physician and outpatient costs and the other for Medicare Part D prescription drug costs.

The HI Trust Fund will contain surplus income through 2027 but is projected to be depleted in 2033, three years earlier than in last year’s report. At that time, revenue would pay only 89% of the program’s costs. Overall, projections of Medicare costs are highly uncertain.

The SMI Trust Fund accounts for Medicare Parts B and D are expected to have sufficient funding because they are automatically balanced through premiums and revenue from the federal government’s general fund, but financing will need to increase faster than the economy to cover expected expenditure growth.

Note: The One Big Beautiful Bill Act, signed into law on July 4, 2025, may impact the Social Security and Medicare programs by reducing the income taxes on Social Security benefits that flow into the OASI and HI trust funds. Although the law did not change the rules for taxing Social Security benefits, the new senior deduction ($6,000 for single filers, $12,000 for joint filers) is likely to reduce the number of people who pay taxes on their benefits and reduce the marginal tax rate for those who do pay taxes. One estimate suggests that this could move the expiration dates for the OASI and HI trust funds up to 2032.2

Possible fixes

If Congress does not take action, Social Security beneficiaries might face a benefit cut after the trust funds are depleted, based on this year’s report. Any permanent fix to Social Security would likely require a combination of changes, including some of these.

- Raise the Social Security payroll tax rate (currently 12.4%, half paid by the employee and half by the employer). An immediate and permanent payroll tax increase to 16.05% would be necessary to address the long-range revenue shortfall (or to 16.67% if the increase started in 2034).

- Raise the ceiling on wages subject to Social Security payroll taxes ($176,100 in 2025).

- Raise the full retirement age (currently 67 for anyone born in 1960 or later).

- Change the benefit calculation formula.

- Use a different index to calculate the annual cost-of-living adjustment.

- Tax a higher percentage of benefits for higher-income beneficiaries.

Addressing the Medicare shortfall might necessitate a combination of spending cuts, tax increases, and cost-cutting through program modifications.

Based on past changes to these programs, it’s likely that any future changes would primarily affect future beneficiaries and have a relatively small effect on those already receiving benefits. While neither Social Security nor Medicare is in danger of disappearing, it would be wise to maintain a strong retirement savings strategy to prepare for potential changes that may affect you in the future.

You can view a combined summary of the 2025 Social Security and Medicare Trustees Reports and a full copy of the Social Security report at ssa.gov. You can find the full Medicare report at cms.gov.

All projections are based on current conditions, subject to chan ge, and may not come to pass.

1) National Institute on Retirement Security, 2024

2) Committee for a Responsible Federal Budget, June 27, 2025

This content has been reviewed by FINRA.

Prepared by Broadridge Advisor Solutions. © 2025 Broadridge Financial Services, Inc.

©2025 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts”) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated through application of the analytical tools and data provided through ycharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or sell, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. For further information regarding your use of this report, please go to: ycharts.com/about/disclosure

RISK DISCLOSURE: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability, or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

SECURITY REMINDER: E-mail transmission may not be secure. If you would like to be contacted by other means please alert Paragon Financial Advisors. By your use of email, Paragon Financial Advisors assumes you agree to our transmission of information by e-mail. Please do NOT send Social Security numbers or account numbers, confidential or privileged information via E-mail.

CONFIDENTIALITY NOTICE: All e-mail sent to or from this address will be received or otherwise recorded by Paragon Financial Advisors and is subject to archival, monitoring or review by, and/or disclosure to the Securities and Exchange Commission. This email and any files transmitted with it are confidential and are intended solely for the use of the individual or entity to which they are addressed. This communication represents the originator’s personal views and opinions, which do not necessarily reflect those of Paragon Advisors. If you are not the original recipient or the person responsible for delivering the email to the intended recipient, be advised that you have received this email in error, and that any use, dissemination, forwarding, printing, or copying of this email is strictly prohibited. If you received this email in error, please immediately notify info@paragon-adv.com

Category

© 2026 Paragon Advisors, LLC. All rights reserved. | Site Credit: Kasey S Consulting