Fed’s June 2025 Rate Pause Explained

July 3, 2025

Why No Change Amid Cooling Inflation & Fed Dot Plot Projections

Introduction

The Federal Reserve’s June 2025 meeting ended with a collective pause, no rate hike or cut, even as inflation has cooled markedly from last year’s highs. Headline CPI has fallen to ~2.4% (core ~2.8%) as of June, a dramatic improvement from 2023’s 6%+ readings. Yet the Fed held the benchmark rate steady around 4.25–4.50%.

Why stand pat when price pressures are easing? The answer lies in the Fed’s cautious outlook, reflected in the Fed dot plot projections and recent macro developments.

Why This Topic Matters Now: Fed Dot Plot Projections & Market Impact

This moment represents a potential inflection point in monetary policy. After an aggressive hiking cycle and a plateau in rates, the Fed is at a crossroads between declaring victory over inflation or erring on the side of restraint.

The June 2025 decision, and the Fed’s own dot plot projections, provide critical clues about the second half of 2025.

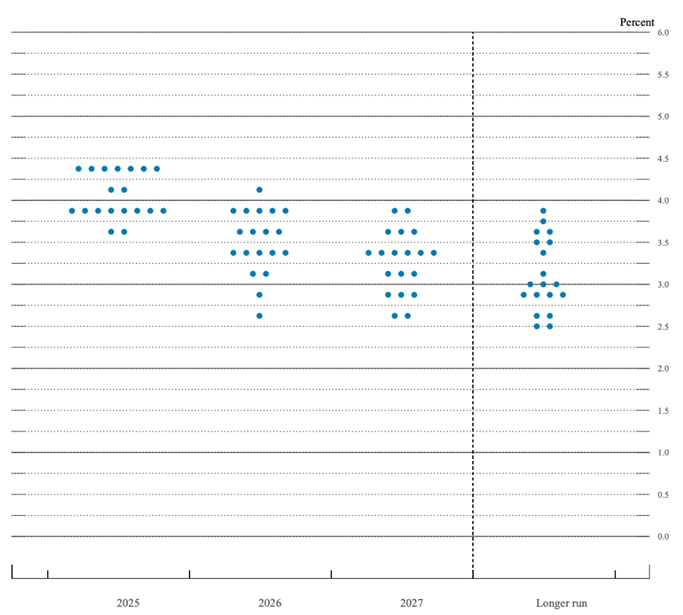

Mixed Signals on Future Rates

Markets have been betting on rate cuts later in 2025. Fed Funds futures pricing showed ~65% odds of at least one cut by September.

However, the Fed’s June dot plot sent a more tempered message. The median projection still shows no rate cuts until late 2025, and even then only about two quarter-point reductions by year-end.

Notably, 7 out of 18 FOMC members foresee no change at all in 2025 — a hawkish tilt that diverges from market expectations.

Cooling Inflation vs. New Inflation Risks

Yes, inflation is falling — a key reason many expected the Fed might start signaling easier policy. But the context of that cooling is critical.

Core inflation at ~2.8% is still above the 2% target. In early June, the U.S. reintroduced tariffs on over $200B in key imports. These tariffs could raise import costs and nudge inflation back up in coming months.

Fed Chair Jerome Powell acknowledged this risk, noting in his press conference that while May’s inflation readings showed “noticeable cooling,” prices may increase in coming months as tariffs take effect.

Macro Turning Point

Economic growth is slowing. The Fed trimmed its 2025 GDP forecast to 1.4%, down from 1.7%.

Meanwhile, the labor market remains solid (unemployment ~4.2%) but is showing subtle signs of softening. We have a late-cycle mix of cooling inflation and moderating growth.

The Fed’s dual mandate requires balancing inflation and employment. By standing pat, the Fed signals it’s prioritizing inflation control over boosting growth at this juncture.

Market Volatility and Client Concerns

Markets are hanging on every Fed signal in 2025. The Fed’s pause, and hints about future moves, are moving bond yields, stock valuations, and even currency trends.

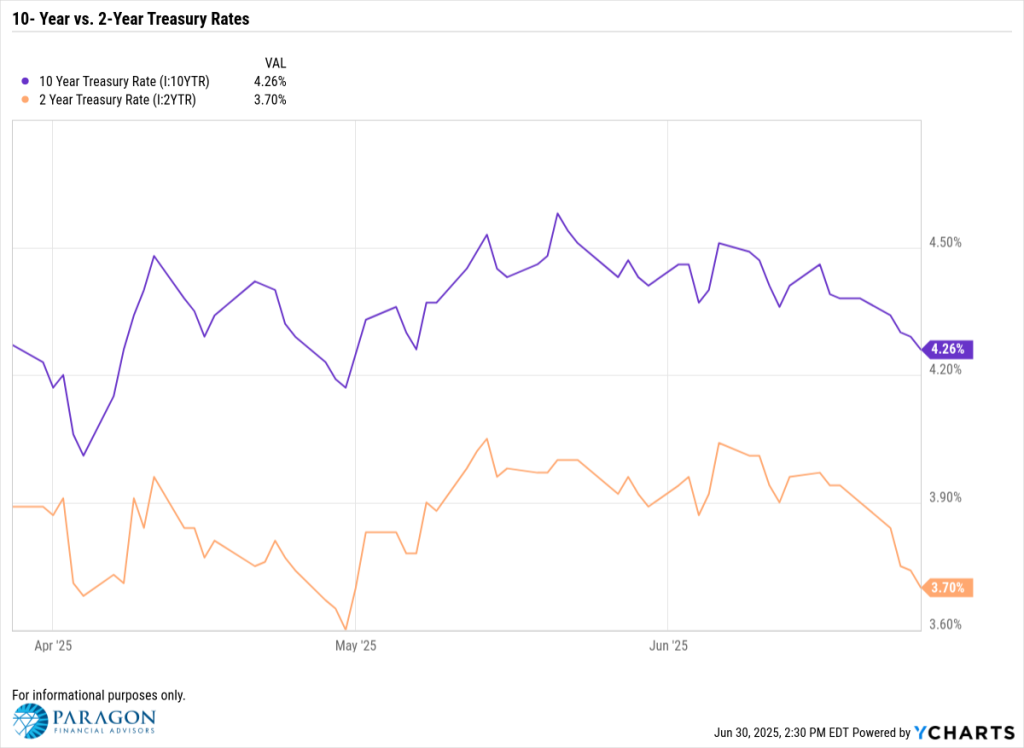

The U.S. Treasury yield curve has been extraordinarily sensitive to Fed expectations. Going into the June meeting, the 10-year yield hovered around 4.4% while the 2-year was near 3.9%.

After the Fed’s no-hike decision and somewhat hawkish projections, long-term yields stabilized instead of plunging. This suggests the market believes the Fed may stay higher for longer.

Equity markets likewise gyrated. Stocks initially rallied on the pause, then pulled back as Powell emphasized “sticky” inflation above 2% and uncertainty around tariffs.

Conclusion: Fed Dot Plot Projections Confirm Patience, Not Passivity

The Federal Reserve’s June 2025 decision to hold interest rates steady — despite clear evidence of cooling inflation — reflects a strategy rooted in patience, not passivity.

Markets may have hoped for an early pivot, but the Fed’s message was clear — progress on inflation is encouraging, not conclusive. The central bank needs durability, not just direction.

Disclaimer

©2025 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts”) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated through application of the analytical tools and data provided through ycharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or sell, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. For further information regarding your use of this report, please go to: ycharts.com/about/disclosure

RISK DISCLOSURE: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability, or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

SECURITY REMINDER: E-mail transmission may not be secure. If you would like to be contacted by other means please alert Paragon Financial Advisors. By your use of email, Paragon Financial Advisors assumes you agree to our transmission of information by e-mail. Please do NOT send Social Security numbers or account numbers, confidential or privileged information via E-mail.

CONFIDENTIALITY NOTICE: All e-mail sent to or from this address will be received or otherwise recorded by Paragon Financial Advisors and is subject to archival, monitoring or review by, and/or disclosure to the Securities and Exchange Commission. This email and any files transmitted with it are confidential and are intended solely for the use of the individual or entity to which they are addressed. This communication represents the originator’s personal views and opinions, which do not necessarily reflect those of Paragon Advisors. If you are not the original recipient or the person responsible, be advised that you have received this email in error, and that any use, dissemination, forwarding, printing, or copying of this email is strictly prohibited. If you received this email in error, please immediately notify info@paragon-adv.com

Category

© 2026 Paragon Advisors, LLC. All rights reserved. | Site Credit: Kasey S Consulting