How Markets Absorb Geopolitical Uncertainty

March 19, 2026

How Markets Absorb Geopolitical Uncertainty Over Time

Periods of geopolitical uncertainty bring financial markets into the spotlight as investors scramble to determine the impacts on their portfolios. The role of financial advisors is amplified as headlines pile up and fear begins to influence how clients interpret short-term market moves.

Looking at the effects of major conflicts over the past several decades helps contextualize moments like today. History shows that while market reactions have not been uniform, short-term volatility has often given way to more constructive long-term outcomes.

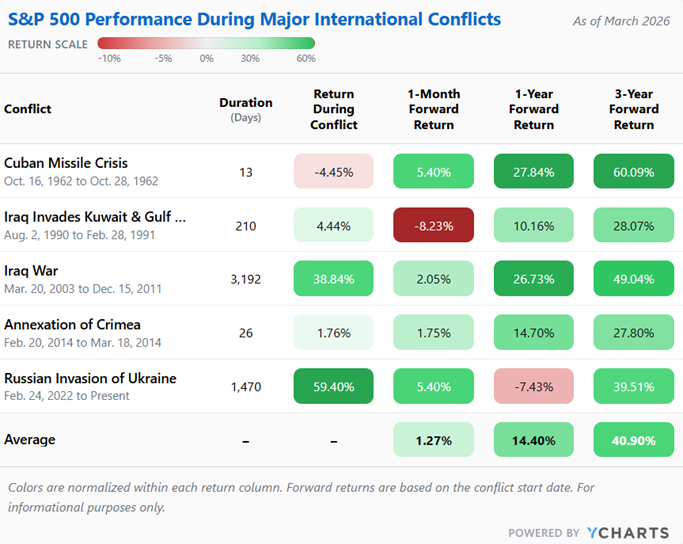

What Past Conflicts Reveal

The length, severity, and market reaction tied to international conflicts can vary. While these periods feel heavily influential as they happen, markets have historically absorbed them alongside broader economic forces.

They can stretch across multiple administrations, shifting rate environments, and entirely separate economic factors, which makes zooming out especially useful for advisors and clients alike.

In the immediate 12 months after these events unfolded, the S&P 500 returned an average of 14.4%, outperforming its long-term average of 10.75%. Three years removed, and the market would have returned a minimum of 27%.

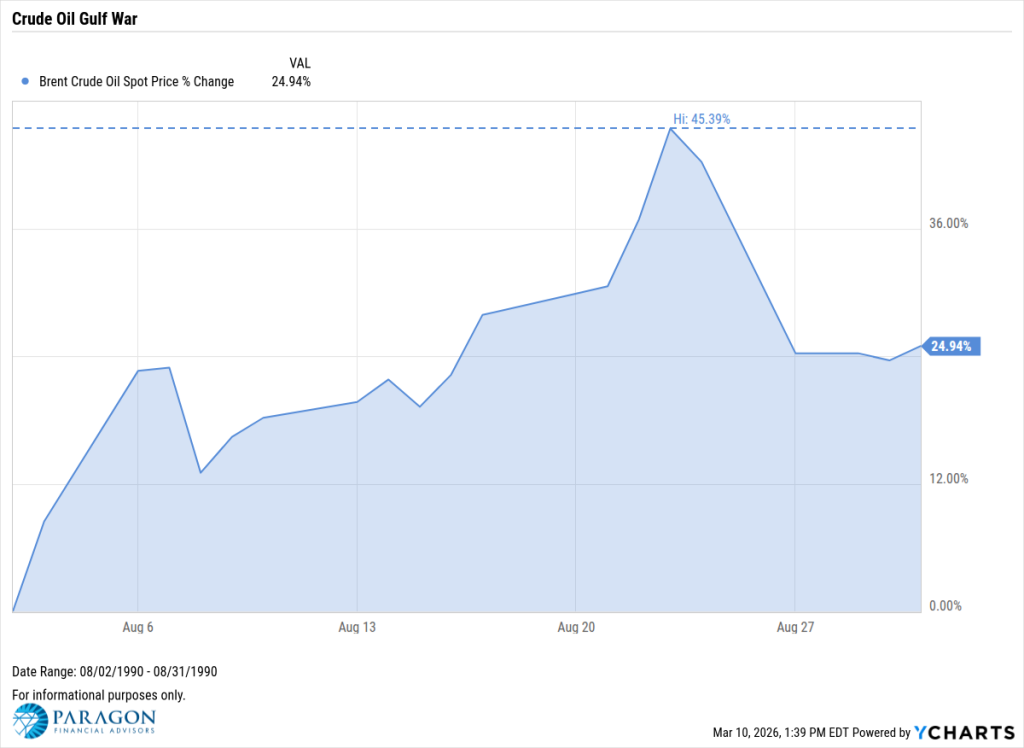

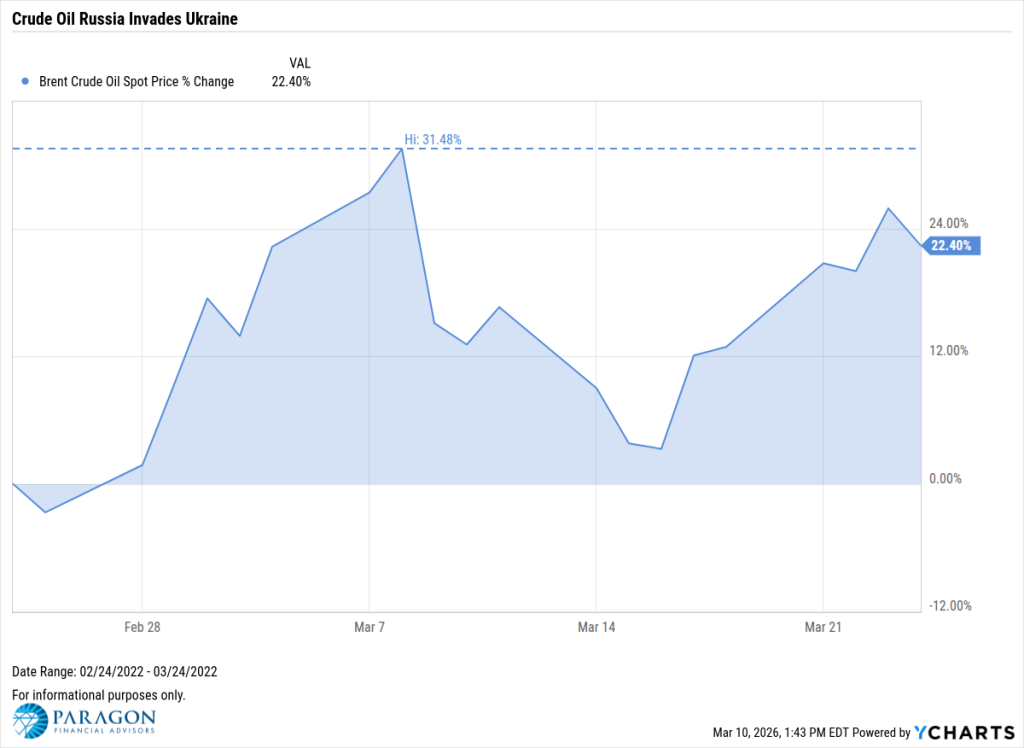

Oil Responds First

Oil consistently experiences the sharpest responses when conflict breaks out in major energy-producing regions, as markets quickly price the risk of disrupted supply and transportation.

During the opening month of the Gulf War, Brent Crude rose as high as 45%, climbing to $32.25 per barrel as markets reacted to regional supply uncertainty.

Following the Russian invasion of Ukraine, Brent again surged, rising above $133 per barrel and finishing the first month more than 22% higher.

To no surprise, the same pattern has emerged in the first week following strikes on Iran. In the past five trading days, Brent Crude is up 25.6% and has crossed $90 per barrel for the first time since October of 2023.

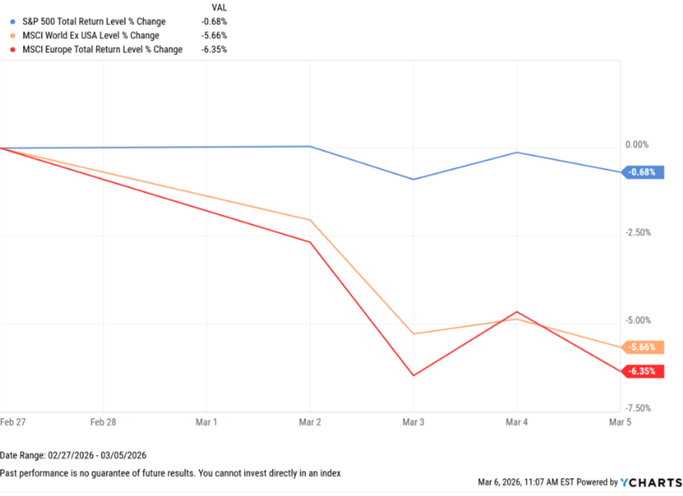

Where International Pressure Builds

This pressure often reaches equities more quickly outside the United States, where higher energy costs carry broader economic implications.

The MSCI European Index fell 6.45% this past week, its biggest weekly decline since April 4, 2025, and its fifth worst week since the March 2020 pandemic drop of -20.28%. This sensitivity reflects Europe’s greater reliance on imported energy, where higher oil prices can feed more directly into production costs, transportation, and growth expectations.

The US, by contrast, benefits from larger domestic energy production and an economy that can gradually absorb these pressures. The S&P 500 has remained more stable, down less than 1%, though underlying sector moves have been far more pronounced.

Dispersion Beneath the Index

Within U.S. equities, divergence is often one of the clearest reminders that periods of geopolitical uncertainty do not affect markets evenly.

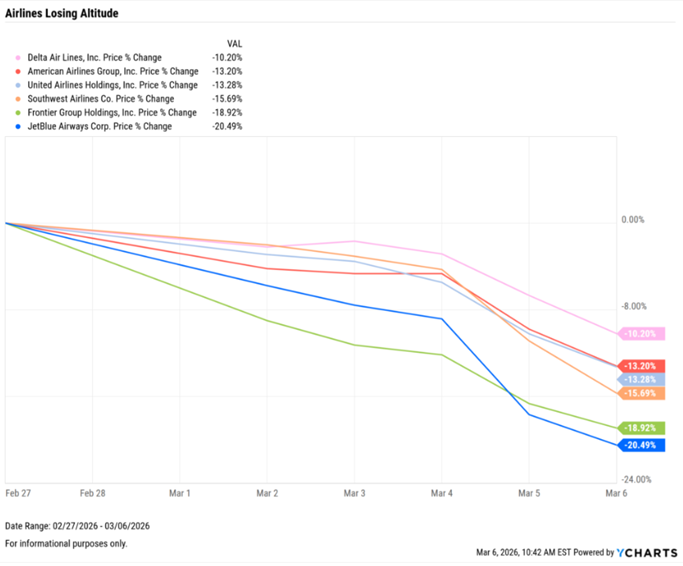

Industries tied more directly to fuel costs, supply chains, or government spending expectations tend to react first as pressure or opportunity emerges. Major airline stocks have come under pressure as higher fuel costs begin to weigh on operating expectations.

At the same time, select defense and government-linked names have moved higher, with Lockheed Martin and Northrop Grumman both up 2%, while Palantir is up over 14%.

While uncertainty around the length and severity of the current conflict remains, history continues to favor investors who stayed disciplined through periods of geopolitical stress.

Oil prices, international equities, and sector-level moves all deserve attention as they influence broader economic sentiment, but markets have repeatedly moved beyond this initial shock period.

Disclaimer

©2026 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts”) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated through application of the analytical tools and data provided through ycharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or sell, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. For further information regarding your use of this report, please go to: ycharts.com/about/disclosure

RISK DISCLOSURE: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability, or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

SECURITY REMINDER: E-mail transmission may not be secure. If you would like to be contacted by other means please alert Paragon Financial Advisors. By your use of email, Paragon Financial Advisors assumes you agree to our transmission of information by e-mail. Please do NOT send Social Security numbers or account numbers, confidential or privileged information via E-mail.

CONFIDENTIALITY NOTICE: All e-mail sent to or from this address will be received or otherwise recorded by Paragon Financial Advisors and is subject to archival, monitoring or review by, and/or disclosure to the Securities and Exchange Commission. This email and any files transmitted with it are confidential and are intended solely for the use of the individual or entity to which they are addressed. This communication represents the originator’s personal views and opinions, which do not necessarily reflect those of Paragon Advisors. If you are not the original recipient or the person responsible, be advised that you have received this email in error, and that any use, dissemination, forwarding, printing, or copying of this email is strictly prohibited. If you received this email in error, please immediately notify info@paragon-adv.com.

SECURITY REMINDER: E-mail transmission may not be secure. If you would like to be contacted by other means please alert Paragon Financial Advisors. By your use of email, Paragon Financial Advisors assumes you agree to our transmission of information by e-mail. Please do NOT send Social Security numbers or account numbers, confidential or privileged information via E-mail.

Category

© 2026 Paragon Advisors, LLC. All rights reserved. | Site Credit: Kasey S Consulting