Paragon Perspectives – 2022 Recap, 2023 Outlook, Risks, and Opportunities

January 3, 2023

With a volatile 2022 in the books and numerous uncertainties looming in 2023, we’d like to provide you with our annual Recap, Outlook, Risks, and Opportunities.

2022 Recap

- To describe 2022 as unprecedented may seem foolhardy, especially in comparison to the economic severity of the Great Financial Crisis or Great Depression, or relative to the inflation rates of the 1970’s, but the magnitude of COVID-induced policies and the velocity of their effects created a perfect storm unlikely any other time in history.

- In December 2021, when interest rates were at 0%, the Federal Reserve presidents, largely considered the wisest economists in America, expected to raise interest rates to 0.9% by December 2022. Instead, 2022 ended with seven rate hikes at 4.33%. Never before had their one-year interest rate expectations been off by more than a factor of two, let alone four.

- By March of 2022, the Fed, still asleep at the wheel, continued injecting excess liquidity, flaming the fires of dangerously high inflation. Upon realizing their misstep, they pivoted and immediately began reducing the amount of money in circulation by $95 billion per month. This sudden reversal in policy (expectations) sent shockwaves through the markets.

- In 2022, inflation peaked at 9.1% in June while core inflation peaked at 6.6% in September. Both measures were the highest in 40 years.

- As the Fed raised rates and sapped liquidity from the economy, 30-year mortgage rates rose from 2.6% in January to 6.5% ending December, peaking at 7.1% in November, the highest in 20 years. The result has been a significant slowdown in housing activity and falling home prices, the first time since the fallout of the Great Financial Crisis.

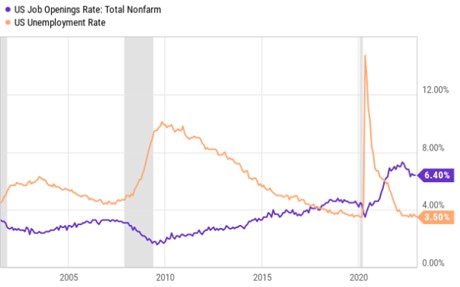

- Unemployment, an imperfect number, is still the most widely tracked measure of employment. It fell from 4.0% to 3.5% in 2022. While unemployment sits exactly at pre-COVID levels, the true number of workers is significantly lower. The lack of participation is not due to employers’ efforts to hire either. Job openings still outnumber those wanting to fill them by nearly two-fold, an incredibly rare and historic imbalance. While many opine on the reasons for such low participation, often focusing on social or qualitative factors, the root cause is based in supply and demand imbalances from legislative intervention.

- While low unemployment makes inflation more difficult to tame, more workers should lead to an increase in supply, largely offsetting each other from an inflation perspective. Wage growth, on the other hand, is an increase in disposable income without a corresponding increase in supply (the same employee output now costs more). This creates a dangerous, self-fulfilling cycle often leading to “stagflation” or the increase in prices without an increase in productivity. For these reasons, the Fed’s greatest concern and most difficult challenge in 2023 will be cooling wage growth. Though the pace has slowed from 5.4% in January to 4.6% in December, it remains above trend and too close to current levels of inflation.

- To only blame the Fed for rampant inflation and crumbling markets would be an unfair assignment of guilt. As much as the Fed should have acted differently, so should have legislators and consumers too. As has always been the case, consumers are near-sighted, impulsive, and categorically spenders over savers. Legislators know this and realize what’s best to get re-elected is rarely what’s best for the voters, at least long-term. Some grace should be extended to the Fed, currently charged with picking up the pieces of too much money sent and spent, on too many things consumers shouldn’t have been able to afford. While the decline in spending warranted some stimulus, the amount provided was unquestionably too much:

- Subsidies such as extended welfare benefits, rent relief, tax credits, stimulus checks, artificially low interest rates, and student loan deferment have provided little incentive to re-enter the workforce. Beginning in October and still ongoing, California even went to the extent of sending up to $1080 pre-loaded on gas debit cards to “offset” their deliberately high cost of gas. This only helped spur demand, it did nothing to lower the cost or increase supply. The result: an even higher cost of living. Do not be fooled; reliance upon the government is the exact outcome desired from purposeful legislation.

- Subsidizing anything creates more demand without the corresponding production of more supply. More demand for the same amount of supply leads to higher prices, this is economics 101. When government intervention is minimal, supply and demand can naturally find an equilibrium that both minimizes prices while maximizing production. Studies have consistently shown this to be the case in states such as Texas and Utah. Until subsidies subside, or supply increases, prices will continue to rise.

- The cumulative result of bad legislative policy, impulsive consumers, and lethargic Fed action led to an unprecedented amount of wealth destruction. Diversification did little to protect investors as there were few places to hide. After accounting for inflation, 2022 was the worst year for stocks since 2008 (the Great Financial Crisis), the worst year for retiree portfolios since 1932 (the Great Depression), and the worst year for bonds ever recorded (going back over 180 years).

- A silver lining does exist to the experiment gone wrong that was America’s overreaction and irrational response to COVID-19, so long as voters are willing to recognize and learn from it. As consumers and politicians cheered their lockdowns and short-lived stimulus as a success, stock markets and home values soared, both largely benefitting the (already) wealthiest of Americans. Wages have failed to keep up with inflation and will certainly not recover the damages already done. Home affordability, which mainly impacts lower income first-time homebuyers, is half where it was pre-COVID and at the lowest level since 1985. In other words, buying a home is more expensive today than any other time most first-time buyers have been alive. The plunge in affordability will likely keep around 70% of would-be buyers renting. This amounts to over three million families each year missing out on one of America’s best wealth stabilizers and creators, homeownership.

- So, what’s the silver lining, you may ask? Time and again, but never to this scale, history has proven there are dire consequences to heavy-handed government intervention, and those most negatively affected long-term are the ones hoping for a short-term solution. Quick fixes are just that, short-lived, but long-term investment in people, businesses, education, and local economies are the proven answers to weathering any storm. Just as we learned from our actions that led to the Great Depression and Great Financial Crisis, this too is a hard lesson learned, yet hope exists that next time things will be different.

2023 Outlook

- More uncertainty. While inflation does appear to have peaked, the pace of decline has been disappointing, forcing the Fed to maintain their aggressive path forward.

- Increasing workforce participation should bring greater supply online, helping reverse the demand imbalance that currently exists.

- Energy and input costs are down dramatically, which should reinvigorate long-term investment, adding to sustainable growth.

Asset Class Returns – Next 5 Years

- Investment returns are mean-reverting; yearly returns can vary greatly but long-term returns are very consistent. Historically the best yearly returns follow the worst ones. In the “Modern Era” of investing (which goes back to 1957), after a 20% decline, the S&P 500 rises, on average, 15% in the following year and returns 29% after three years (and has only had a negative return once).

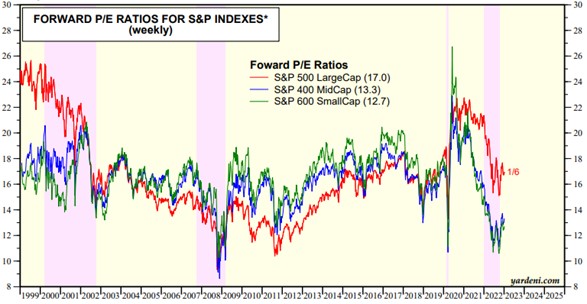

- We believe the market is underestimating the durability of corporate earnings and their optionality to cut costs, increase prices, or withstand an economic slowdown; we see compelling value in most areas of the stock market. Specifically, small cap and growth stocks, which now trade below their 5% and 10% historical valuations, respectively. Small caps trade at the steepest discount to large caps since 2001 and growth trades at the closest relative valuation to value since 2009. Below are the performance differences since these relative valuations last occurred. While prior returns are no guarantee of future performance, we believe the recent underperformance of each has gone too far.

- In last year’s report we believed traditional bonds, specifically Treasuries, were the most overvalued asset class, relative to other available options such as real estate or floating-rate bonds. Now that the bubble has burst in truly epic fashion (long-term treasuries fell over 40% last year), yields are sitting well above decade-highs. We believe the market is too pessimistic on bonds in light of declining inflation and slowing economic growth. In periods of true distress (not record low unemployment and 5% wage growth), such as 2008 or early 2020, long-duration Treasuries returned over 40%. As investor focus shifts from inflation to economic slowdown, we believe a focus on quality over valuation will return.

- Finally, our outlook for private or alternative investments is slightly less optimistic. Last year we highlighted them as our favorite given their ability to absorb inflation or simply because they’re not subject to the daily repricing of their publicly traded peers. After a battering in 2022, we believe public investments provide a more compelling relative valuation than this time last year. If public assets remain depressed for longer than we expect, private investments would likely play “catch up (down)” as they are slowly valued lower.

Risks

- We see two primary risks in 2023, each relating to inflation and each impacting two groups of people differently. We define the group who are retired or have sizeable portfolios as “Wall Street” given their dependence on investment performance. Those early in their careers or rely on a strong job market are more closely related to “Main Street.” As is often the case, the same event impacts Main Street and Wall Street differently.

- The most dangerous risk to Wall Street is strong consumer demand keeping inflation stubbornly high. Additional legislative missteps, such as student loan forgiveness or further expansion of federal programs, have proven to be strong drivers of consumer spending and the bane of taming inflation. It is estimated over 80% of all household COVID stimulus has already been spent with less than 20% going towards debt repayment or savings. Any additional stimulus would likely follow suit. If consumers continue paying higher prices for the same discretionary goods and services, inflation will continue to rise. This would lead to higher interest rates lasting longer than expected. As was the case throughout 2022, stocks and bonds sold off each time.

- The second risk we see is the exact opposite and is a greater risk to Main Street America. The Fed going too far or for too long with their aggressive tightening would likely lead to greater damage to households than is otherwise necessary to bring down inflation. To minimize economic damage a pivot to more accommodative policy would likely follow. Long-term unemployment would rise, wage growth would slow, and the US could return to pre-COVID’s sub-par growth. While certainly undesirable for Main Street, investments have historically thrived in a low interest rate environment.

- Given Fed decisions made today are based on data often over a year old (as is the case with slow-moving rental inflation), the impact of today’s actions will not fully be known till at least a year from now. Since inflation and wage growth is already dangerously high, it’s like the Fed is attempting to drive in reverse, well above the speed limit, using only the review mirror for guidance. Inevitably, reactionary mistakes will happen. The Fed has a track record of overshooting in both directions, too slow to react then too aggressive in response. For this reason, we believe the second risk is more likely than the first.

- As households come to terms with the financial toll of 2022 they may become more risk-adverse at exactly the wrong time. This can be a very serious risk to the long-term success of meeting one’s goals and objectives. We follow the proven practice of increasing risk during market declines (buy low) and de-risking when assets reach a peak (sell high). While buying before the selloff is over can magnify the pain, as was the case in 2022, it is very likely to help recover faster than doing nothing, as was the case in 2020. As Warren Buffet said, (be) “fearful when others are greedy and greedy when others are fearful.” This is our investment philosophy.

Opportunities

- The silver lining to many aspects in life, especially those driven by emotion, is peak pessimism always precedes a brighter future. Nearly every investment asset class is cheaper today than a year ago. The current selloff has increased future expected returns significantly, which are historically very strong after a significant decline. The following page shows BlackRock’s expected returns for various asset classes over the next five years. The first is current as of September 2022 and the second is from September 2021 and included in last year’s report. With the exceptions of Buyout and Real Estate, all other asset classes have higher expected returns.

- While real estate, goods, and services remain expensive, nearly all publicly traded assets are quite cheap, at least against their historical valuations. According to Morningstar, stocks have only been this cheap 5% of the time, the last two being March 2020 and 2009, both of which preceded strong investment returns. While most households cannot change their core living expenses, they can decide where excess money goes. If 2022 has impacted your standard of living, consider delaying large discretionary purchases in favor of prioritizing your retirement savings.

- Do you have tax-deferred retirement accounts? Roth conversions are a great way to boost your retirement savings on an after-tax basis. Many investments are down significantly and converting these from a tax-deferred account to Roth would allow the future recovery to be tax-free. While taxes would be due on the conversion the long-term result is almost always a net benefit. We recommend discussing any taxable events with your tax professional.

- Ending on a positive note, inflation has had a positive impact on your future taxes. The same level of income in 2023 will be taxed at a lower effective rate since income brackets and standard deductions have expanded, allowing more income to be taxed at a lower rate. Similarly, you can now set aside more for retirement than last year. If you’d like to know how these impact your personal situation, please let us know.

While sticking to the financial plan is rarely easy, history has shown it is the best path to long-term success. We understand any concerns you may have after such a turbulent year. Please know we’re always here, readily available to discuss.

From the entire Paragon Team, we’d like to thank you for your trust in allowing us to serve you. We’re excited to see what 2023 brings and hope to meet with you soon.

Category

© 2026 Paragon Advisors, LLC. All rights reserved. | Site Credit: Kasey S Consulting