Why are Treasury Yields Rising in 2025?

February 27, 2025

Why Treasury Yield Are Rising in February 2025?

In February, Treasury yields have experienced an upward trajectory as investors respond to higher-than-anticipated inflation data and concerns over proposed U.S. import tariffs. The 10-year Treasury yield, a critical benchmark for fixed-income investors, has risen to 4.56%, reflecting market adjustments to these economic indicators. Let’s dive into some key factors and learn what they mean.

Key Takeaways

10-Year Treasury Yield: Increased to 4.56%, its highest level since late 2024.

2-Year Treasury Yield: Rose to 4.94%, maintaining an inverted yield curve, which often signals recession concerns.

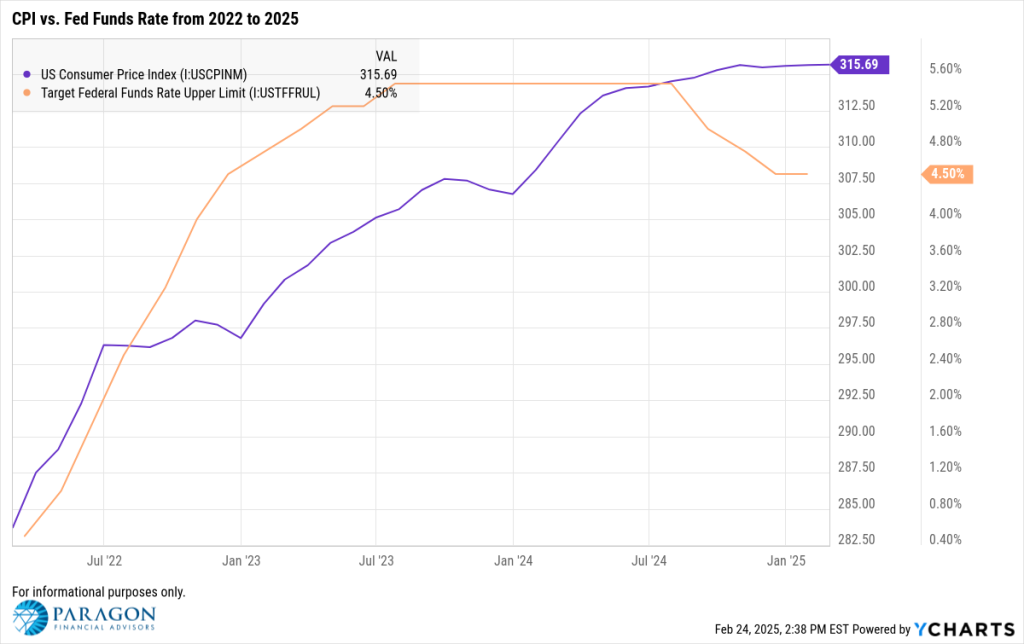

Inflation Impact: January CPI data showed a 3.0% YoY increase, surpassing expectations and potentially delaying anticipated rate cuts by the Federal Reserve.

Tariff Concerns: Proposed tariffs on imports, including steel and aluminum, have introduced uncertainty regarding economic growth and inflation.

Treasury Yield Trends Over the Last 12 Months

Initially, the 10-2 Year Treasury Yield Spread (difference between 10-Year and 2-Year yields) was negative, indicating that the 2-year yield was higher than the 10-year yield at the beginning of the period in February 2024.

The yield spread began to narrow throughout 2024 and turned positive in September 2024, suggesting an inversion had been corrected as the 10-year yield increased relative to the 2-year yield.

By the end of the period, the spread remained positive and stabilized around 0.25% to 0.31% in early 2025.

Why Treasury Yields Are Rising: Inflation & Tariff Uncertainty

1. Inflation Exceeds Expectations, Delaying Rate Cut Hopes

The January 2025 CPI report revealed that inflation rose by 0.5% on a seasonally adjusted basis, leading to a 3.0% year-over-year increase. This uptick in inflation suggests that the Federal Reserve may postpone any rate cuts previously anticipated for the near future.

Key Data Points:

Core CPI (excluding Food & Energy): Increased by 0.4% in January, with a 3.3% year-over-year rise, indicating persistent inflation in sectors such as shelter and services.

Shelter Costs: Rose by 0.4% month-over-month, continuing to exert upward pressure on overall inflation.

2. Treasury Yields Respond to Tariff Concerns

The administration’s recent proposal to reinstate Section 232 tariffs on imports, particularly targeting steel and aluminum, has added complexity to the economic landscape.

Potential Effects on Treasuries:

Inflationary Pressures: Tariffs on imported goods can lead to higher consumer prices, contributing to sustained inflation.

Economic Growth Uncertainty: Trade tensions may dampen business investment and consumer spending, potentially slowing economic growth and increasing demand for safe-haven assets like Treasuries.

Disclaimer

©2024 YCharts, Inc. All Rights Reserved. YCharts, Inc. (“YCharts”) is not registered with the U.S. Securities and Exchange Commission (or with the securities regulatory authority or body of any state or any other jurisdiction) as an investment adviser, broker-dealer or in any other capacity, and does not purport to provide investment advice or make investment recommendations. This report has been generated through application of the analytical tools and data provided through ycharts.com and is intended solely to assist you or your investment or other adviser(s) in conducting investment research. You should not construe this report as an offer to buy or sell, as a solicitation of an offer to buy or sell, or as a recommendation to buy, sell, hold or trade, any security or other financial instrument. For further information regarding your use of this report, please go to: ycharts.com/about/disclosure

RISK DISCLOSURE: Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

This material is for information purposes only and is not intended as an offer or solicitation with respect to the purchase or sale of any security. The content is developed from sources believed to be providing accurate information; no warranty, expressed or implied, is made regarding accuracy, adequacy, completeness, legality, reliability, or usefulness of any information. Consult your financial professional before making any investment decision. For illustrative use only.

SECURITY REMINDER: E-mail transmission may not be secure. If you would like to be contacted by other means please alert Paragon Financial Advisors. By your use of email, Paragon Financial Advisors assumes you agree to our transmission of information by e-mail. Please do NOT send Social Security numbers or account numbers, confidential or privileged information via E-mail.

CONFIDENTIALITY NOTICE: All e-mail sent to or from this address will be received or otherwise recorded by Paragon Financial Advisors and is subject to archival, monitoring or review by, and/or disclosure to the Securities and Exchange Commission. This email and any files transmitted with it are confidential and are intended solely for the use of the individual or entity to which they are addressed. This communication represents the originator’s personal views and opinions, which do not necessarily reflect those of Paragon Advisors. If you are not the original recipient or the person responsible for delivering the email to the intended recipient, be advised that you have received this email in error, and that any use, dissemination, forwarding, printing, or copying of this email is strictly prohibited. If you received this email in error, please immediately notify info@paragon-adv.com

Category

© 2026 Paragon Advisors, LLC. All rights reserved. | Site Credit: Kasey S Consulting